Technology has moved from being tangential to a company’s strategic departments to one that is central. Insurers are looking at the potential value they can leverage by investing in technology that can help them sell more, manage risk better and drive down operation costs by empowering agents to do more in less time.

In the 2024 trends, we have updates on the direction insurance technology spending will take. This is an interesting shift from the market projections in 2021 that showed that CIOs were keen to spend up to 3.7% of premiums on technology (Novarica’s Insurer IT Budgets and Projects 2021)

"Insurers should consider the potential value they can create by using technology to sell more, manage risk better, and cost less to operate overall, rather than treat technology as an expense to be managed to historical norms." - Matt Josefowicz, Novarica president and CEO

A global survey by Deloitte of 200 CIOs found that 48 percent agreed that their companies did not have the technological capabilities to navigate the changing markets. This sentiment is what drove increased technology investments as companies begin to undergo digital transformation to become more agile and scalable.

According to a Forbes prediction for 2024, based on 2023 trends, insurance IT spending is expected to witness a 5% hike. Increased insurance technology spending will be aimed at addressing customer experience (CX) enhancements and strengthening foundational capabilities. Insurers are faced with the challenge of balancing seemingly conflicting objectives, including enhancing CX, boosting revenue, and cutting costs. In the coming year, technology teams are expected to allocate investments strategically to areas that effectively address all three priorities.

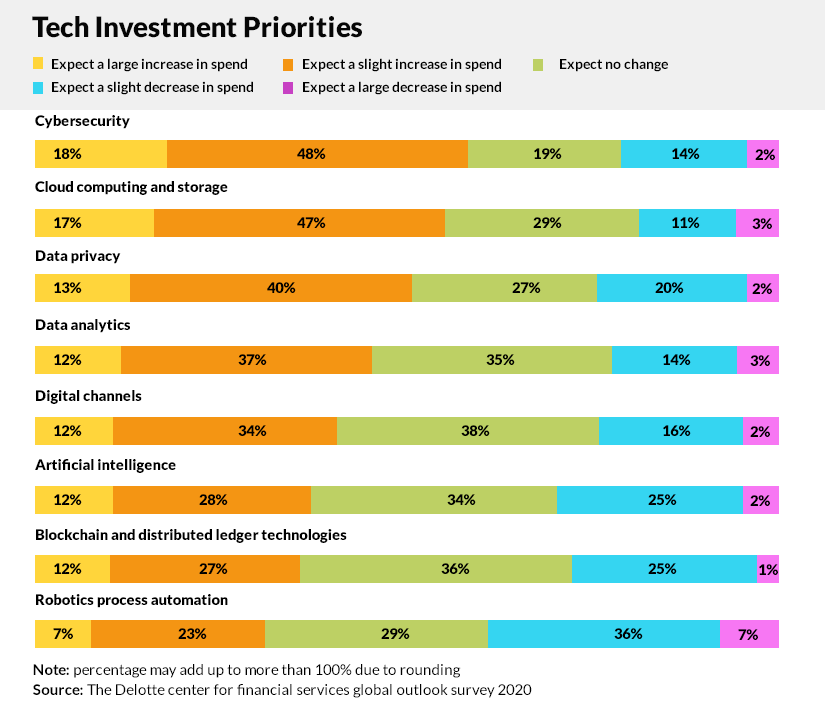

Freeing up capital for technology investments: 2024 vs 2021

The property and casualty (P&C) industry, recognized for intense competition and slim profit margins, faced heightened challenges during the global pandemic economic downturn. As the impact waned, P&C insurers grappled with rising costs due to inflation, particularly in goods affecting personal insurance claims.

Specifically, in auto insurance, supply chain disruptions led to a significant 22.8 percent increase in the cost of vehicle parts and equipment between June 2021 and June 2022. Moreover, car insurance rates soared by 17% in the first half of 2023.

Looking ahead to 2024, the insurance sector, especially P&C insurance, is gearing up for a digital transformation. By embracing new technologies and innovative business models, insurers aim to proactively navigate current challenges and shape the industry's future.

In 2021 Insurance companies began to explore new avenues to reduce overall operational costs. This was critical to make up for revenue shortages in 2020 and to divert resources towards long-term investments for digitization in insurance. In 2021 there were 2 main ways CIOs were planning to go about this: by mapping current workflows to identify any redundancies or unnecessary expenses, by reviewing upcoming investments and delaying ones that were not immediately critical, or by a combination of the two. This strategy continues to hold true with a 30% increase in the rate of adoption of new AI/ML projects from 2021 to 2022.

The adoption rate has surged significantly, with a direct increase of 30% in new AI/ML projects from 2021 to 2022 (Insurance Thought Leadership)

The insurance sector has evolved alongside economic developments. With each significant technological leap, the industry has adapted by introducing new products, innovative distribution methods, and enhanced risk assessment approaches. The past decade alone has witnessed more technological innovation than the preceding five decades combined

-

Automation: Automating manual repetitive processes can free up valuable time for insurance agents, reduce agent headcount, and prevent costly mistakes that can arise from human error.

-

Artificial intelligence: Like automation, artificial intelligence will play a key role in developing lean, cost-effective workflows. In customer service departments, for example, Generative AI can handle a bulk of incoming queries, leaving only the most complex ones for human reps to resolve. This means a scalable, cost-effective team, happier customers, and less churn. There are challenges with the use of AI as new regulations stress on transparency to avoid bias.

-

Embedded insurance: Looking ahead to the insurance landscape of 2024, there is the possibility of significant opportunity and potential challenge posed by the rapid expansion of embedded insurance. Though the concept isn't new, there has been an increasing marketing of insurance premiums into third-party transactions. This trend has the potential to disrupt traditional channels.

If insurance is embedded 70% of customers in the 18 to 34 age group are more inclined to purchase it from a consumer brand.

Telematics: Auto insurance, currently centered on individual driver risk, will eventually need to adapt to address the technological risks linked to fleets of autonomous vehicles and potentially privately owned autonomous vehicles (AVs). This shift implies that insurance coverage may need to transition from focusing on drivers to encompass automakers and software companies responsible for developing and maintaining various autonomous driving technologies.

Also Read: Why Implementations Often Cost Millions and Take 18 Months or More?

Key avenues for digitization in the insurance sector

Work-from-home in 2021 became the new norm for companies across the world, and the insurance sector needed to find a way to move from on-premise facilities to flexible remote setups. Even as we have moved back to a more hybrid approach, the shift in tech investments has accelerated because of the insights gained.

In a nutshell, CIOs still plan to invest heavily in three key areas:

Cloud technology and digital transformation

Cloud migration was the next big avenue of growth long before the pandemic, but 2020 certainly acted as a catalyst in its adoption. Suddenly as tens of thousands of employees were forced to work remotely, insurance companies had to ensure that data was available in a protected environment that could be accessed from any location - something that could only be solved with the cloud. 2024 is likely to see an uptick in investments in digitization in insurance, cloud infrastructure, and continued migration from legacy software.

According to a 2023 study by Arizent, 43% of insurers identified cloud and digital infrastructure as their top priority.

Embracing digital transformation provides digital insurers with a significant edge over traditional carriers by reducing insurance premiums with technology. BCG (Boston Consulting Group) notes this disruptive shift can cut up to 10% in premium costs and 8% in claims expenses.

Cybersecurity

With data moving from one centralized location to the cloud, it’s imperative that security measures are tightened to ensure it remains protected. A Deloitte survey in 2021 revealed that around 66 percent of CIOs globally, believed that there would be an increase in spending on cybersecurity. In 2024, a good part of insurance IT spending will be on AI and ML integration for better information security.

Compliance

As insurers begin to open up access to data and offer more customer-centric features such as self-service portals, there will be an increased focus on compliance. Spending on compliance is also reflective of the new work setups and the cybersecurity focus of insurance firms. Insurtech partners who offer compliant features will become more in demand as the focus on security continues to grow.

In a world where virtual services, IoT integration, and automation are becoming increasingly important, CIOs will have to make several long-term strategies to restructure key areas of the business and kickstart insurance digital transformation.

Topics: Digital Transformation